SPFPL and LBO: structuring the entry into capital and the development of liberal professions

The SPFPL allows liberal professions to structure the entry into capital and the development of their activity according to a logic similar to the LBO.

SPFPL and LBO: structuring the entry into capital and the development of liberal professions

The practice of liberal professions is now part of increasingly structured trajectories. Firms are growing, associations are being renewed and generations are succeeding each other. In this context, many questions arise in a very concrete way: integrating the capital of an existing firm, organizing the gradual withdrawal of historical partners or supporting the growth of an activity without weakening one's personal situation.

To meet these challenges, the law has made specific tools available to regulated liberal professions. The financial participation company for liberal professions, better known under the name of SPFPL, is one of the main ones. Often presented as a simple holding company, it is in reality a structuring financing and organization instrument, whose operation is frequently based on an economic logic similar to a takeover with leverage effect, commonly referred to as an LBO.

The objective of this article is to explain this mechanism in a clear and accessible way, in order to understand its benefits, functioning and points of attention, without going into unnecessary technicality.

The SPFPL, a structure dedicated to liberal professions

SPFPL is a company specifically designed for regulated liberal professions. It does not carry out the professional activity itself and does not replace the firm or the practice company. Its role is To organize the holding of the capital of structures in which professionals actually carry out their activities, in particular self-employed companies.

Placed upstream of the office, the SPFPL acts as a head structure. It constitutes The parent company in legal and fiscal terms. The practice company, in which the activity is carried out on a daily basis, in the daughter company. This distinction is central to understanding the logic of assembly.

The SPFPL thus makes it possible to structure the distribution of capital, governance and financing, while allowing operational activity to take place in an unchanged framework. Although it can adopt a classical legal form, such as an SARL or a SAS, it remains subject to specific rules. The composition of its capital, the quality of its managers and certain structuring decisions are strictly supervised and placed under the control of professional orders, in order to guarantee independence and respect for the ethical principles specific to each profession.

Financing an entry into capital without increasing personal debt

When a liberal professional wants to acquire the capital of an existing firm or take over the shares of an outgoing partner, the question of financing is immediately central. A direct personal acquisition often involves significant debt, with lasting consequences on the private situation.

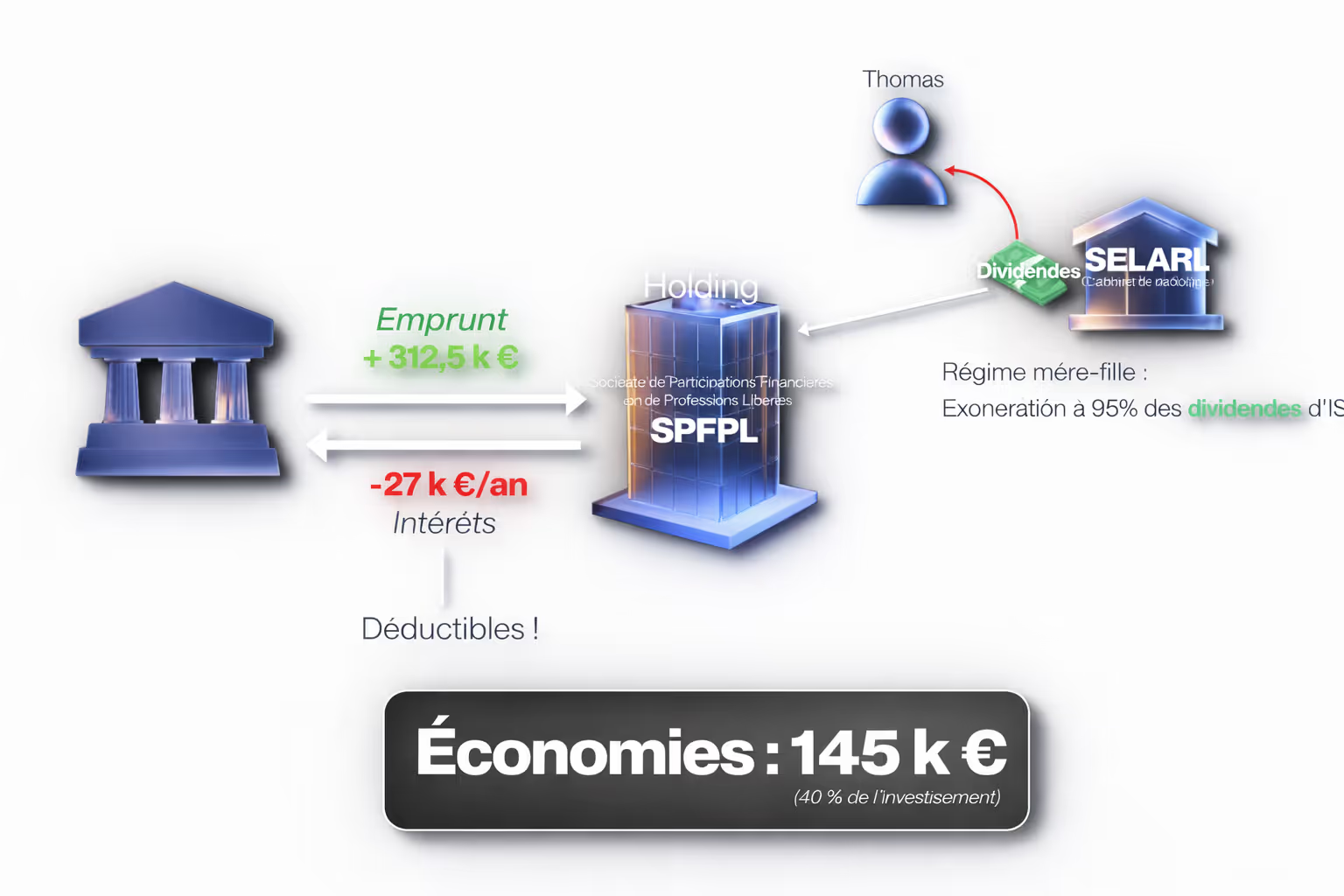

The SPFPL makes it possible to approach this problem differently. The professional creates a structure dedicated to his activity, which becomes the parent company. This SPFPL contracts A bank loan In order to finance the acquisition of the shares of the exercise company, which became the daughter company. The debt is thus borne by the professional holding company and not directly by the natural person.

The schema is based on a simple principle. The SPFPL acquires the shares through the loan. The operating company is continuing its activity and is reporting results. Some of these results are distributed in the form of dividends to the SPFPL, which uses these flows to progressively repay the loan taken out during the acquisition.

This organization can be illustrated by the case of Thomas, a young radiologist. Her journey is shown in more detail in our video.

Rather than acquiring the firm's shares directly in his own name, Thomas chose to create an SPFPL dedicated to his business from the start. This parent company borrowed to finance his entry into the capital of the radiology office, structured in the form of an exercise company. The dividends paid by the firm to the SPFPL then make it possible to ensure the gradual repayment of the debt, within an adapted fiscal framework.

This scheme is based on a guiding idea: to allow the activity itself to finance its development, without excessively exposing the professional in a personal capacity.

An economic logic similar to an LBO

Behind this legal organization is an economic mechanism that is well known in the business world. The acquisition is not financed by prior savings, but through debt. This debt is borne by an intermediate structure and then repaid thanks to the results generated by the activity acquired.

It is precisely this principle that is referred to by the term of buy-back with leverage, or LBO. In an SPFPL scheme, the professional holding company plays the role of the acquisition company, while the practice company is the target company. The flows flow back from the daughter company to the parent company, allowing the gradual repayment of the loan.

The SPFPL thus makes it possible to adapt the LBO logic to the specific framework of liberal professions, while respecting their regulatory and ethical constraints. When properly sized and supported by a profitable business, this type of arrangement is part of a healthy and sustainable economic logic.

It also makes it possible to support the evolution of the firm over time, with the gradual arrival of new partners and the gradual withdrawal of historical partners, without calling into question the balance of the structure.

The decisive role of taxation

The effectiveness of this arrangement is largely based on its tax regime. The SPFPL is subject to corporate tax, This makes it possible to maintain results at the level of the holding company without immediate taxation at the personal level.

Above all, the so-called “mother-daughter” regime allows the dividends paid by the operating company to flow back to the SPFPL with very limited taxation. In practice, only one a flat rate of 5% remains taxable, the balance being exempt.

This reduced taxation makes it possible to allocate most of the flows to the repayment of the loan used to finance the acquisition of the shares. To this partial exemption is added the deductibility of loan interest at the level of the parent company, which further reduces the overall cost of financing.

It is the combination of these two mechanisms that allows an acquisition financed by debt to be balanced over time, as long as the activity generates sufficient results.

Anticipating the medium and long term consequences

The SPFPL remains a supervised tool, designed to meet specific professional objectives. It is not intended to become a wealth holding company that allows you to invest freely or to organize a family transfer without constraints.

Owning capital remains closely linked to the professional quality of the partners, which may limit some options in the long term. In addition, the holding of shares via an SPFPL has consequences in the event of a future sale of the operating company or the reorganization of the capital.

These elements must be integrated right from the reflection phase in order to avoid complex trade-offs at a later stage.

Thus, the SPFPL is now a structuring lever for liberal professions who wish to organize an entry into capital, take over shares or support the development of their business. Its operation is frequently based on a takeover logic with leverage effect, inspired by the LBO, but adapted to a specific professional framework.

When thought out beforehand and implemented methodically, SPFPL makes it possible to reconcile financing, capital organization and legal security. However, it requires a rigorous analysis of the profitability of the activity and an expectation of the medium and long term consequences.

It is precisely in this phase of foresight that the joint intervention of the lawyer and the notary makes perfect sense, in order to secure the set-up from the start and to place the project on a sustainable trajectory.

To go further and illustrate these mechanisms in concrete terms, you can find our analysis on video: https://www.youtube.com/watch?v=y0ME8fUU490&t=1566s

.png)