SCI for income tax or corporate tax: how to make the right choice?

The choice between SCI and IR or IS determines the taxation of rents, resale, transmission and asset structuring of a real estate project.

SCI for income tax or corporate tax: how to make the right choice?

The real estate civil society (SCI) is a central tool for holding and organizing real estate assets, whether it is a family or professional project. The choice between income tax (IR) and corporate tax (IS) is a structuring decision, with lasting fiscal, asset and economic consequences.

A structuring choice since the creation of the SCI

In principle, SCI is subject to income tax. However, it can opt for corporate tax, according to a strict formalism. This choice is neither neutral nor purely technical.

It impacts rent taxation, financing arrangements, accounting management, resale taxation and transmission strategies. It must therefore be assessed in the light of the real estate project as a whole and the wealth horizon of the partners.

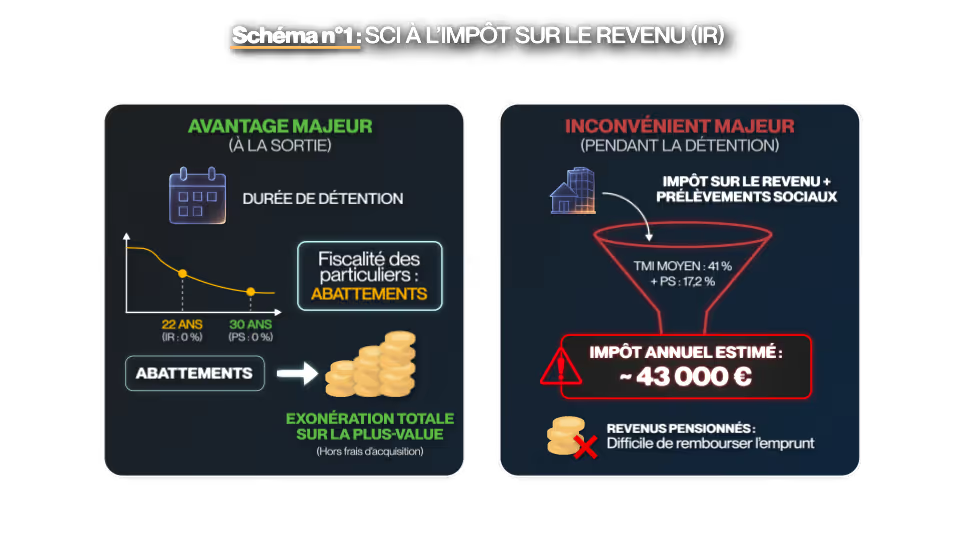

The SCI for income tax: a wealth logic

Subject by default to income tax, the SCI is fiscally transparent. The result is determined at the company level and then taxed directly in the hands of the partners, in proportion to their rights in the capital.

The rents received are taxed in the property income category, according to the marginal tax bracket of each partner, plus social security contributions at the rate of 17.2%.

Some expenses are deductible, including loan interest, maintenance and repair work, property tax, and management fees. On the other hand, the building cannot be depreciated.

In the presence of a land deficit, it can, under conditions, be deducted from the overall income within the annual limit of 10,700 euros, the balance being carried over to future property income.

The major advantage of SCI in IR lies in the taxation of exit. The sale of the building or shares falls under the regime of real estate capital gains for individuals, with allowances for the duration of ownership leading to a total exemption from tax after 22 years and from social security contributions after 30 years.

This regime is particularly suited to long-term ownership and asset transfer strategies.

The SCI in corporate tax: a financial logic

The SCI can opt for corporate tax, provided that it expressly requests it from the tax authorities. This option cannot be tacit or implied.

Once subject to corporate income tax, the company is taxed on its profits at the rate of 15% up to 42,500 euros (under conditions), then 25% beyond that. Partners are only personally taxed in case of distribution of dividends.

The main advantage of this regime lies in the possibility of depreciating the building, excluding the value of the land. Depreciation makes it possible to significantly reduce taxable income and improve returns in the short and medium term.

In return, SCI at IS is subject to comprehensive commercial accounting and strengthened reporting requirements.

The essential consideration appears at the time of the transfer. The capital gain is calculated by the difference between the sale price and the net book value, without any allowance for the duration of ownership. The more the property has been depreciated, the higher the tax base.

The tax is paid by the company, then additional taxation occurs in the event of distribution to the partners. SCI at IS should therefore be reserved for projects that are clearly oriented towards capitalization or long-term holding with no prospect of resale in the medium term.

Practical focus: the case of Thomas

To illustrate these issues in concrete terms, we rely on Finary's video with the case of Thomas, an associate radiologist at a private practice company.

In this scheme, Thomas and his partners create an SCI subject to income tax, owned directly by the practitioners, with the aim of acquiring the premises intended to accommodate medical activity.

Secondly, the usufruct of the shares is transferred, for a fixed period, to the benefit of the operating company. Throughout the duration of the usufruct, it has the economic enjoyment of the premises it occupies.

The benefits for operating activity

This organization ensures the lasting stability of business premises and limits the risks associated with a traditional lease, such as rent renegotiation or non-renewal.

It also makes it possible to secure the work tool and to preserve the independence of the operating structure.

Patrimonial and fiscal effects

From a fiscal point of view, friction remains limited. During the duration of the usufruct, the operating company amortizes the value of the usufruct and deducts the expenses related to the occupation of the premises.

The SCI, remaining subject to income tax, is not concerned by the taxation of professional capital gains. At the end of the usufruct, the partners regain full ownership of the shares without taxation.

In the event of a subsequent transfer of the building or shares, the applicable taxation remains that of individuals, with allowances for duration of ownership and progressive exemption.

Therefore, the choice between income tax and corporation tax for an SCI cannot be decided uniformly.

SCI à l'IR favors simplicity, transmission and favorable exit taxation. SCI at IS responds to a logic of optimizing income and capitalization, at the cost of increased complexity and heavier taxation of sales.

Hybrid schemes, such as SCI to IR with temporary transfer of usufruct of shares, however, make it possible to reconcile operational security and asset construction.

In practice, only a global legal, fiscal and asset analysis makes it possible to select the package that is really adapted to the project being pursued.

To go further and illustrate these mechanisms in concrete terms, you can find our analysis on video: https://www.youtube.com/watch?v=y0ME8fUU490&t=1566s

.png)