The sale of equity shares: tax regime and conditions of application

The sale of equity shares benefits from a preferential tax regime under strict conditions of ownership and participation.

The sale of equity shares: tax regime and conditions of application

The sale of shares is a structuring moment in the career of a manager or associated professional. It generally comes after several years of development and marks a decisive step in the organization of professional and personal assets.

Under French law, the sale of equity shares benefits from a particularly favourable tax regime. Often presented, wrongly, as an almost total exemption from capital gain, this taxation is in reality based on a set of precise conditions relating to the nature of the shares, their duration of ownership and the level of participation in the company sold.

When these conditions are met, the taxation associated with the transfer can be very significantly reduced.

Equity shares are, in principle, held by companies subject to corporate tax. A natural person can never, legally, hold shares qualified as equity securities.

In particular, this concerns holding companies, group parent companies, operational companies with strategic participations, as well as SPFPLs formed within the framework of regulated liberal professions.

The legal form of the holding company is irrelevant. What matters is its corporate tax liability and the economic logic in which the stake was acquired and maintained.

The qualification of equity shares

Equity shares are securities held permanently by a company when such ownership is useful for its activity.

This usefulness may result from the exercise Of an influence or Of a control on the issuing company, but also on the integration of this participation in a economic or professional strategy wider.

Conversely, the titles vested In a logic purely financial or speculative fall under investment securities and are excluded from the diet.

The qualification is assessed at the time of the acquisition of shares. The fact that a stake is subsequently transferred is not incompatible with its nature as an equity title, as long as the original intention and the circumstances of detention reflect a lasting logic.

The conditions for access to the preferential tax regime

The application of the tax regime for equity securities requires compliance with cumulative conditions, which constitute the basis for securing the system.

Securities must first be held since at least two years from the date of transfer. Otherwise, the capital gain is taxed in full at corporate tax at the common law rate.

They must then represent at least 5% of the capital and voting rights of the issuing company. This threshold is the main criterion for access to the regime and allows, subject to other conditions, to also benefit from the parent company regime.

Below this threshold, qualification remains theoretically possible, but it presupposes a reinforced demonstration of the usefulness of detention for the company's activity.

The tax regime applicable to the transfer

When the conditions of ownership and participation are met, the capital gain realized during the sale falls under the regime of long-term capital gains on equity securities.

The capital gain is exempt from corporate tax, except for a fixed share of costs and charges of 12%, reintegrated into the taxable result.

This regime, commonly referred to as” Niche Copé ”, is one of the most favorable tax mechanisms in French law. However, it does not apply to shares of companies with a preponderance of real estate and assumes strict consistency between the legal, accounting and fiscal characterization of securities.

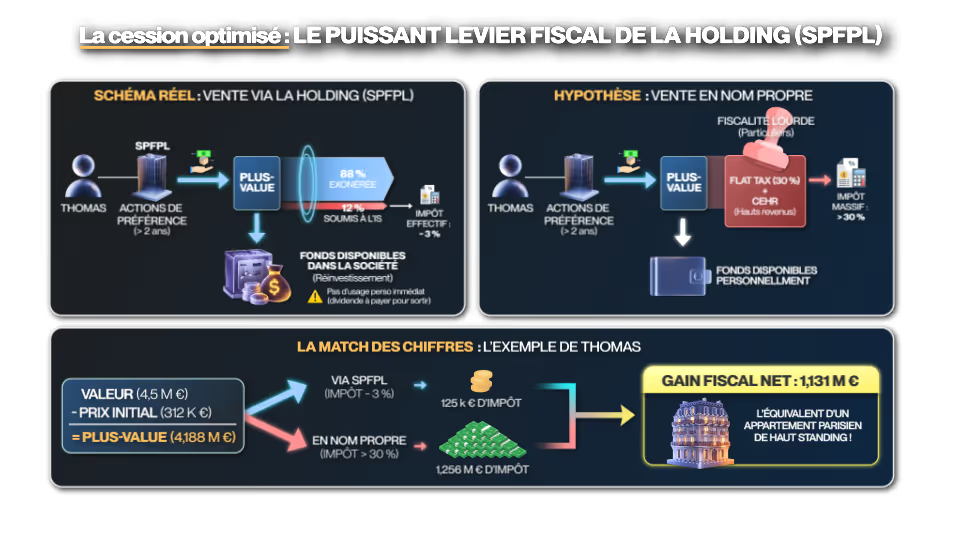

Concrete illustration: sale of shares held via an SPFPL

This analysis focuses on the case of an associate physician whose shares in the practice company are held by an SPFPL subject to corporate tax.

In this configuration, the professional does not directly own the shares. The SPFPL is the legal owner of the shares issued by the operating company. These shares were acquired in a sustainable manner, in direct connection with professional activity, and represent a significant participation in society.

At the time of the sale, the capital gain is realized at the level of the SPFPL and falls under the regime of long-term capital gains on equity securities, with the application of the share of expenses and expenses of 12%.

Conversely, a direct holding by a natural person would have led to the application of the regime of capital gains for individuals, with immediate taxation at the single flat rate of 30%, possibly increased by the exceptional contribution on high incomes.

Transfer taxation that must be prepared in advance

The sale of equity shares illustrates a fundamental principle: the taxation of the sale takes place well before the sale itself.

This regime is neither automatic nor universal. It rewards foresight, economic coherence and long-term structuring

The joint intervention of the lawyer and the notary precisely makes it possible to secure these choices beforehand and to include the transfer in a global asset strategy, adapted to the professional and family objectives of the manager.

To go further and illustrate these mechanisms in concrete terms, you can find our analysis on video: https://www.youtube.com/watch?v=y0ME8fUU490&t=1566s

.png)