Preferred shares and sales in the medical sector

Preference shares make it possible to organize certain transfers in the medical sector, subject to strict compliance with professional independence.

Preferred shares and sales in the medical sector

Divestiture transactions in the medical sector cannot be understood as simple financial transactions. They are part of a specific legal framework, structured around the protection of the professional independence of practitioners, which directly conditions the procedures for opening capital, financing and transferring medical structures.

In this context, preference shares are frequently presented as a tool for reconciling the regulatory constraints specific to health professions with the economic expectations of investors. However, this presentation requires careful reading. While recourse to preference shares is legally possible, it remains strictly regulated and their scope is often misunderstood.

The principle of professional independence and its capitalistic consequences

The law applicable to companies operating in the private practice of medical professions is based on a central principle: the independence of practitioners in the exercise of their art.

This principle aims to ensure that medical decisions, the organization of care and professional strategy cannot be influenced by interests outside the profession. It results in mandatory rules relating to the holding of share capital and voting rights.

The texts require that doctors practising within society keep the majority of capital and decision-making power. In practice, this requirement most often leads to reservations. at least 75% of the capital and the voting rights of practitioners.

The objective is to avoid any takeover, direct or indirect, by third parties who are not doctors and to maintain effective control of the work tool by those who practice the profession. This requirement is a matter of professional public order and cannot be neutralized by simple statutory adjustment.

This constraint has an immediate impact on transfer transactions. Legally, the portion of capital that can be sold to a financial investor is limited. Economically, on the other hand, transfer transactions generally relate to the totality of the group's value, whether in terms of its earnings capacity, its development potential or its long-term value.

It is from this tension between legal constraints and economic reality that the recourse to mechanisms of dissociation between power and value was born.

Preference actions as a tool for dissociation

Preferred shares make it possible, in joint stock companies, to manage the rights attached to the shares forming the share capital.

They allow financial and political rights to be modulated. by way of derogation from the ordinary shares regime, subject to compliance with the rules of public order applicable to regulated professions.

In medical practice companies formed in the form of SELs by shares, this mechanism can be used to organize a differentiated distribution of rights between partners. It makes it possible to distinguish The titles that concentrate decision-making power of those who primarily carry economic value, provided that practitioners maintain effective control of the company and its activities.

Preference actions are therefore not a tool for circumventing professional rules. They should be analyzed as a legal engineering instrument that makes it possible, within certain limits, to articulate the regulations specific to medical professions with economic or asset objectives.

Illustration by a sale transaction in a radiology group

This logic can be illustrated by a planned sale transaction in a radiology group, presented in the video devoted to the heritage career of Thomas, a radiologist.

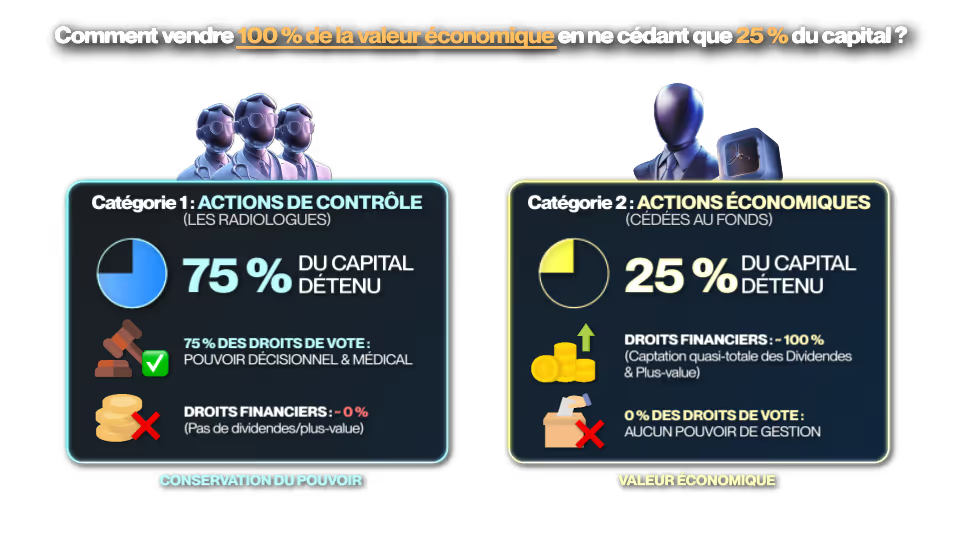

In this type of configuration, the applicable rules require that radiologists maintain 75% of the capital and voting rights of the practice company. The sale to an investment fund can therefore only legally concern 25% of the shares, even though the transaction aims, in economic terms, at the overall valuation of the group.

To meet this constraint, capital is structured into two categories of shares, preferably.

A first category includes preferably so-called control actions. These actions represent 75% of the capital and voting rights. They are owned by the group's radiologists. They allow them to practice the profession within the structure, to participate in strategic decisions and to maintain control of medical organization and professional governance. In return, these actions are voluntarily poorly endowed with financial rights.

A second category corresponds to so-called economic shares, preferably. These actions represent 25% of the capital. They do not confer voting rights on medical management decisions and do not allow any interference in professional activity. On the other hand, they concentrate most of the financial rights, whether it is the dividends distributed by the company or the capital gain realized during the sale.

It is these preferential economic shares that are sold to the investment fund. The fund thus captures almost all of the economic value of the group, while radiologists retain the majority of the capital and all of the medical power, while continuing their activity within the structure.

The limits and risks of these arrangements

Such an arrangement is based on a delicate balance.

The ordinal authorities, the tax authorities and the judge are not limited to a formal reading of the statutes or to the qualification given to the titles. They appreciate The economic reality of relationships between partners and the concrete effects of editing on professional independence.

When the financial rights granted to an investor are such that they create excessive economic dependence or that they indirectly influence strategic or organizational choices, the risk of being called into question becomes real.

Preference actions should never have the effect of depriving practitioners of effective control of their work tools.

In practice, these arrangements require an extremely precise drafting of the statutes, a global coherence between governance, the organization of the activity and financial flows, as well as a perfect match with professional requirements.

Preference shares are a legal tool powerful buts closely framed in medical practice societies.

In certain configurations, they can make it possible to organize an economic transfer while respecting the rules of holding capital and power. However, their effectiveness depends less on their legal sophistication than on their adequacy with the reality of professional practice, the governance put in place and the wealth trajectory of practitioners.

To go further and illustrate these mechanisms in concrete terms, you can find our analysis on video: https://www.youtube.com/watch?v=y0ME8fUU490&t=1566s

.png)